Executive summary

- This a major geopolitical escalation but with contained market spillovers so far.

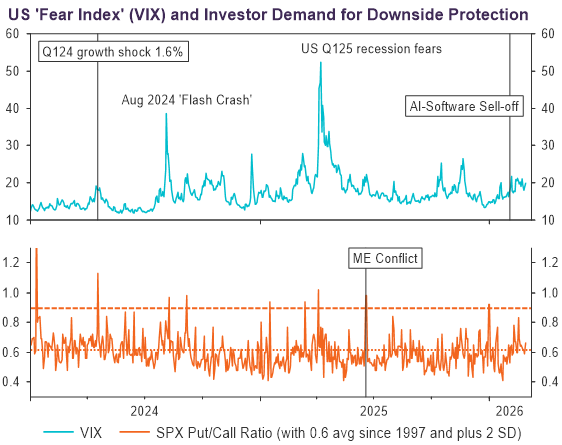

- There is heightened risk aversion in the near-term. But investors’ demand for protection (as seen from the Put / Call ratios on the S&P 500) are still lower compared to the Middle East crisis in June 2025.

- The expected scenario of increased appetite for safe haven assets (higher gold prices, lower US treasury yields, a higher USD), as well as elevated energy prices is playing out.

- We see limited impact on structural inflation from energy prices. Improved productivity from technological and AI adoption will keep longer-term cost pressures in check.

- We are maintaining our 12-month constructive outlook on risk assets, underpinned by ample liquidity, a robust global growth environment, productivity-led gains, and rising incomes.

- Gulf Cooperation Council (GCC) bonds have responded in an orderly manner so far – sentiment may be moderating but fundamentals are intact. Areas with strong sovereign linkages continue to be viewed as fundamentally sound. We do not see immediate liquidity or credit concerns at this stage.

- Historical trends suggest that geopolitical shocks typically normalise once the extent of the disruption becomes clearer.

What happened?

On February 28, Israel along with support from the US, launched a massive military assault across various sites in Iran – taking out its leader Ali Khamenei, and other senior leadership personnel in the process. Iran responded with missile strikes on several US military assets in various Gulf States, and also in targets close to civilian populations. With other Gulf States being attacked, this risks a wider conflagration across the region. Moreover, with Iran’s leadership in disarray, there could be a power vacuum for some time to come, which impacts its response coordination and the length of this conflict.

Heightened risk aversion in the short-term. Constructive on risk assets over the next 12-months

Given escalating tensions and the fluid situation, the heightened risk premium is reflected, especially in oil prices: Brent has jumped by 9% to USD 79.42 / barrel1, following supply disruptions, infrastructure impairment concerns, and lower shipping volumes along the Straits of Hormuz. However, other risk metrics are still much lower than last year’s Middle East crisis – especially the VIX Fear Index and investors’ demand for downside protection (as gauged from the put / call ratio trend on the S&P 500) – see Figure 1 below. The typical short-term impacts are an elevated US dollar, lower bond yields and higher gold prices – all these have unfolded so far.

Figure 1: Measured VIX levels and subdued put / call ratio demand for S&P 500

Source: LSEG Datastream, March 2026

We expect any shocks from higher oil prices on inflation to be short-lived. Oil price pressures may not be as extreme as some fear because the environment today is very different. Supply growth is much stronger in global oil markets than demand at present. Global oil supply flexibility, combined with the credibility of US military and political backing, can help mitigate any significant and sustained oil price pressures. Improved productivity from technological innovation and rapid AI adoption are also expected to keep longer-term cost pressures in check.

Specific to Gulf Cooperation Council (GCC) bonds, USD credit markets in this space have responded in an orderly manner so far, with risk sentiment softening but fundamentals largely intact. Middle East banks with strong sovereign linkages continue to be viewed as fundamentally sound, supported by robust government balance sheets, with no immediate liquidity or credit concerns evident at this stage. Conversely, more cyclical or higher-beta sectors including certain real estate and consumption-linked names may face greater scrutiny as investors re-assess risk premia under a fluid geopolitical backdrop.

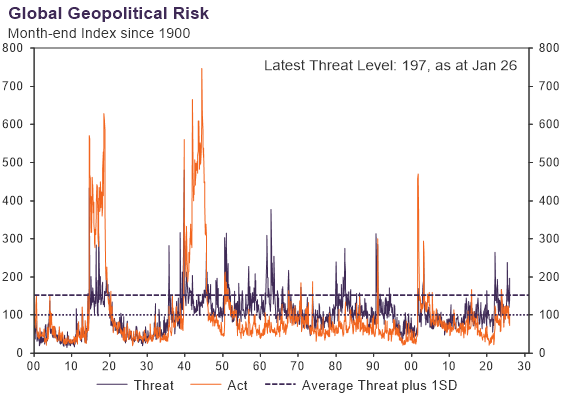

We maintain our 12-month positive outlook for risk assets – underpinned by ample liquidity, a robust global growth environment, productivity-led gains, and rising incomes (which supports wealth-backed spending). See our Q1 2025 FIV, Global Exceptionalism with the 4Rs for reasons as to why we hold a constructive view for global risk assets. Geopolitical shocks can be concerning, but thus far global investors have taken recent developments in their stride, largely because the credibility of the US’ military actions (and outcomes) remains high. See Figure 2 below suggesting contained global geopolitical risk versus historical spikes, and investors increased adaption to navigating higher threat levels for some time now.

Figure 2: Media count of geopolitical threats and actions since 1900

Source: LSEG Datastream, February 2026

Notwithstanding that this is a fluid geopolitical development, Israel and the US remain very credible military powers – further enhanced by the US actions in Venezuela earlier this year, and now with the swift elimination of Iran’s Supreme Leader Ali Khamenei.

Concluding thoughts

Historical precedence suggests that geopolitical shocks typically often normalise once the extent of disruption becomes clearer. Should the current conflict be short-lived and energy flows continue largely uninterrupted, risk premia could gradually re-trace and allow markets to re-focus on underlying economic fundamentals, which are still robust.

(Date: 2 March 2026)

1 Source: LSEG Datastream, March 2026.

Important Information

No offer or invitation is considered to be made if such offer is not authorised or permitted. This is not the basis for any contract to deal in any security or instrument, or for Fullerton Fund Management Company Ltd (UEN: 200312672W) (“Fullerton”) or its affiliates to enter into or arrange any type of transaction. Any investments made are not obligations of, deposits in, or guaranteed by Fullerton. The contents herein may be amended without notice. Fullerton, its affiliates and their directors and employees, do not accept any liability from the use of this publication. The information contained herein has been obtained from sources believed to be reliable but has not been independently verified, although Fullerton Fund Management Company Ltd. (UEN: 200312672W) (“Fullerton”) believes it to be fair and not misleading. Such information is solely indicative and may be subject to modification from time to time.

The audio(s) have been generated by an AI app