Executive summary

- Wealth levels in Singapore have risen over the past decades from domestic build-up and from foreign inflows.

- Despite the rising affluence, Singaporean households have large cash holdings and are “under-invested” in financial assets (including domestic equities).

- With greater deployment of this “dry powder” and increased participation in local equities, this could enhance trading activity, liquidity, and valuations.

- Foreign inflows have been rising due to Singapore’s appeal for political stability, the rule of law, and its reliable regulatory environment.

- Along with the city’s access to top-tier financial, legal, and wealth management services, this has led to a more vibrant ecosystem.

- With a deeper domestic capital market, the opportunities may expand beyond the traditional income and blue-chip space.

Background

Blue-chip stocks may come to mind when thinking about investing in Singapore.

But as we examined more closely the broader trends shaping Singapore today, the next phase of opportunities in the market would likely come from outside blue-chips.

See our reasons why we think so here, Beyond Singapore blue chips: the next chapter in SG equities.

One important shift brewing in the background is the growing wealth pool in Singapore.

Household incomes, property values, and CPF savings have helped build domestic wealth, while Singapore’s status as a global wealth hub has also attracted capital from abroad.

This could support stronger liquidity, greater investor participation, and rising interest in Singapore equities.

In earlier articles, we discussed the structural reasons for investing in Singapore now and highlighted sectors beyond the blue chips that could benefit from these trends.

Here, we take a closer look at another facet of the narrative: how rising wealth levels (domestic and foreign) are re-shaping the opportunity sets in Singapore stocks.

Rising household wealth and under-investments suggests more “dry powder” for deployment

#1 – Average household wealth is rising in Singapore

According to the Ministry of Finance’s first comprehensive household wealth report published in February 2026, resident households in Singapore held an average net wealth of S$1.76 million in 20231.

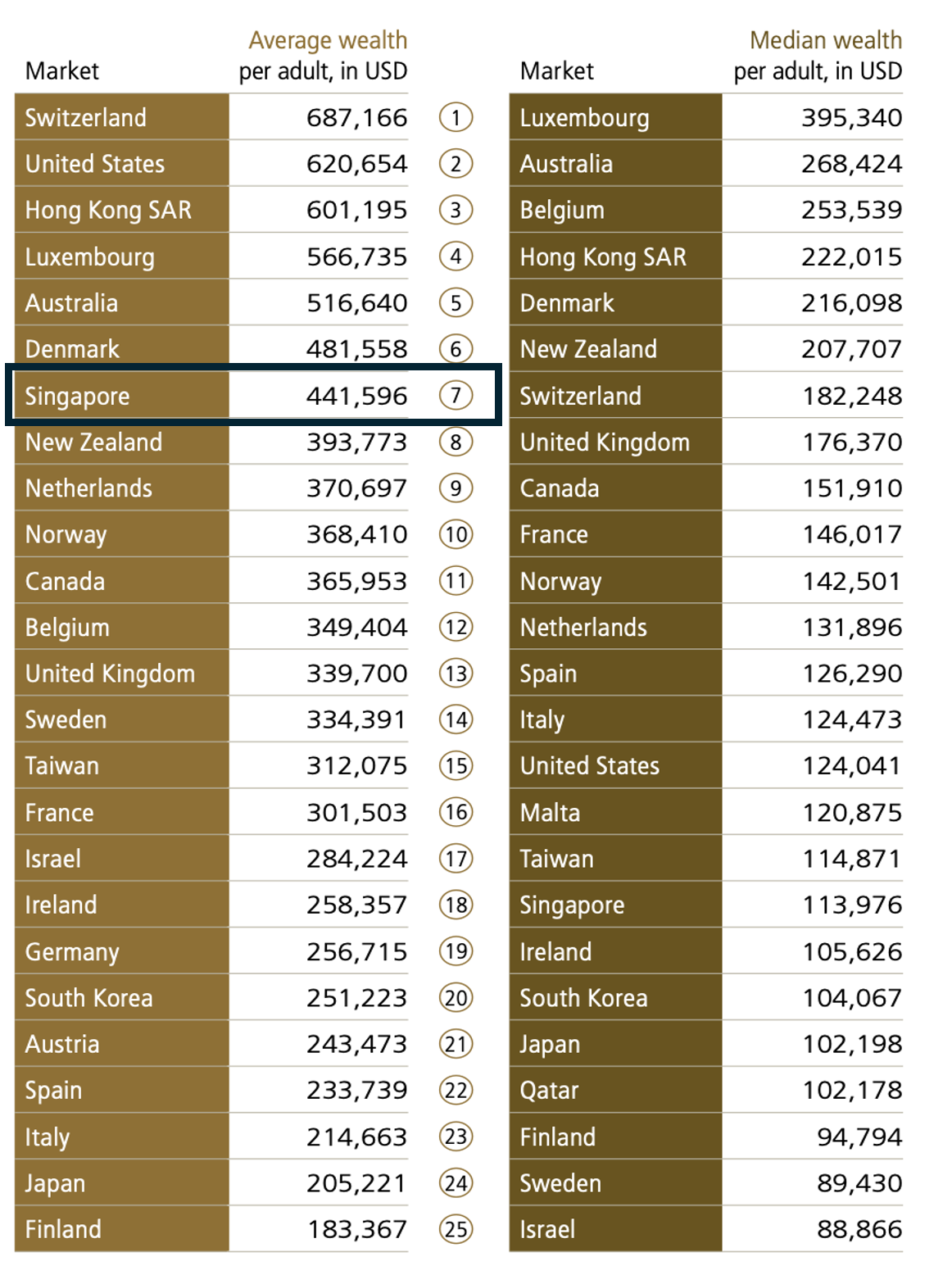

Further, Singapore ranks 7th globally by average wealth per adult, according to the UBS Global Wealth Report 2025, ahead of major economies such as Canada, the United Kingdom, Germany, and Japan2.

Figure 1: Wealth per adult – “The Global Top 25” (Singapore ranked 7th)

Source: UBS Global Wealth Report 2025, calculation based on OECD data, complemented by International Monetary Fund (IMF), United Nations (UN), World Bank Group (WBG) data, and national statistics offices data.

With Singapore’s rising position as a wealth hub in Asia, resulting from converging prosperity both domestically and from inbound capital flows, this is leading to a more vibrant investment ecosystem.

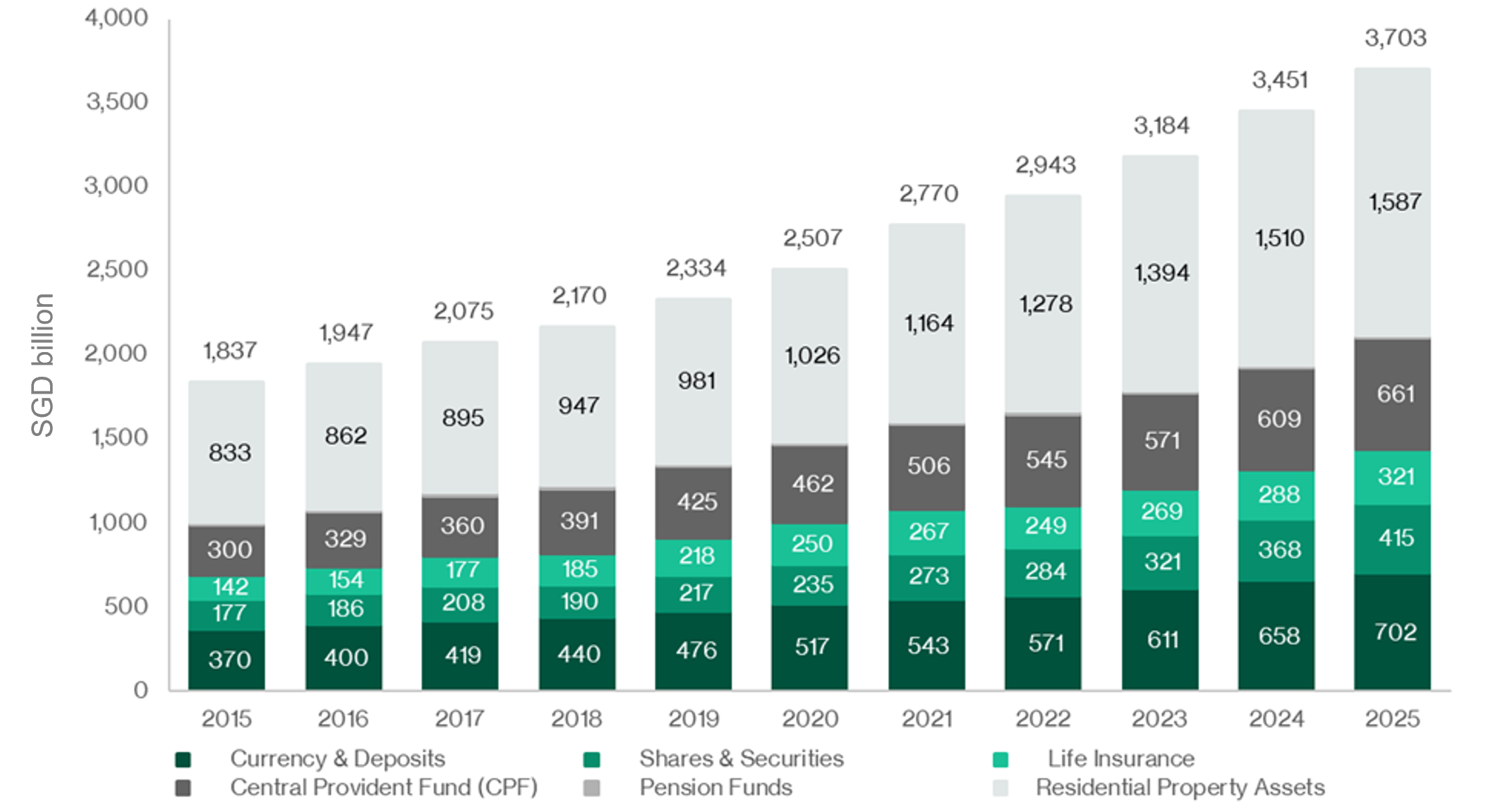

Figure 2: Singapore’s household assets by type – significant amounts in currency & deposits for potential “deployment”

Source: Department of Statistics (DOS), February 2026.

Singapore’s domestic wealth has been built mainly through employment income, investment income, property ownership, and long-term savings.

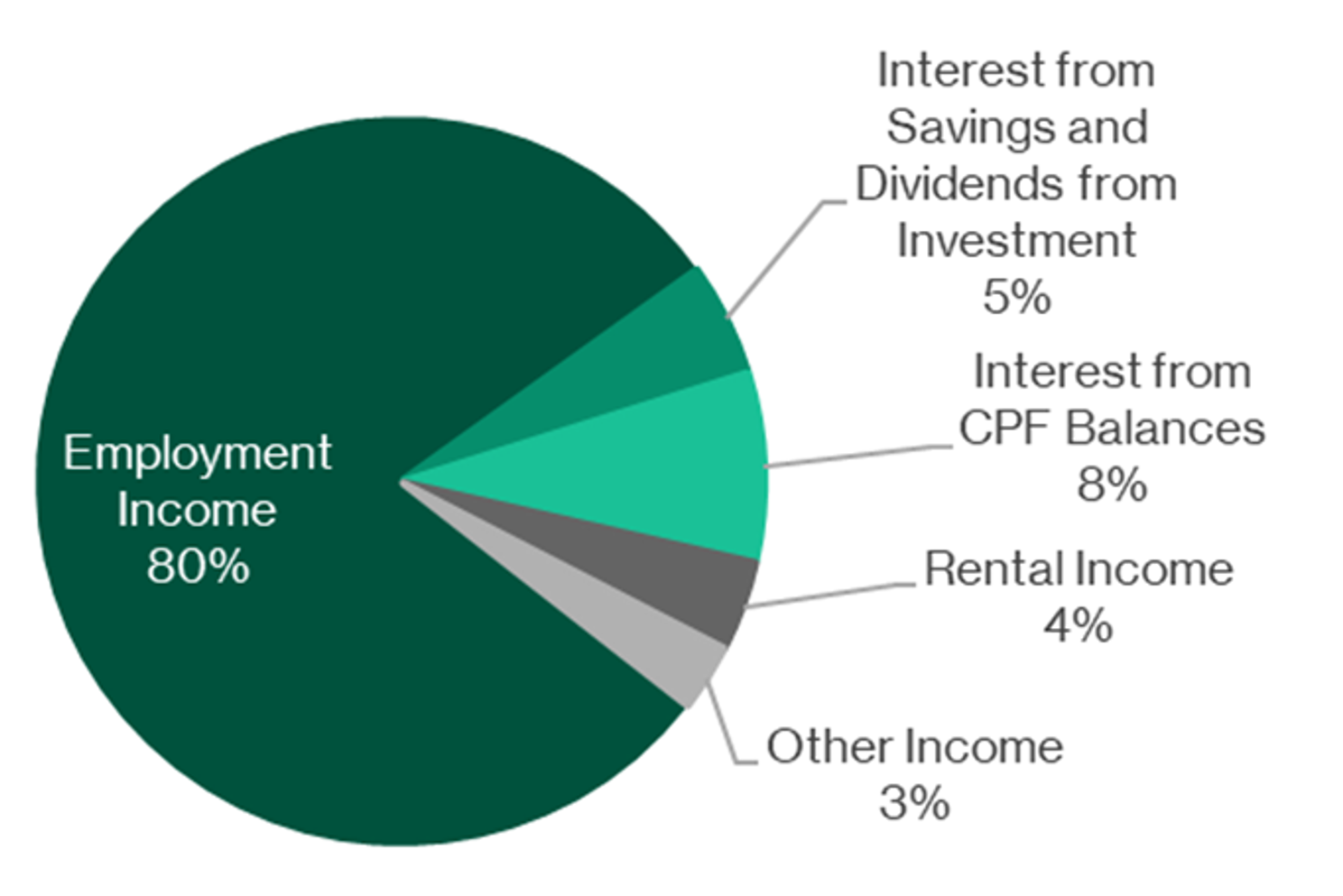

In 2025, employment income (including self-employed business owners) accounted for 80 percent of average monthly household income, showing that wages and salaries remain the main engine of wealth creation.

Other income sources are smaller contributors, with CPF interest contributing 8 percent, dividends and savings interest 5 percent, rental income 4 percent, and other (largely investment) sources 3 percent3.

Collectively, this reflects decades of strong savings habits, entrepreneurial spirit, rising property values, and a CPF system that has supported long-term financial planning.

Figure 3: Average monthly Singapore household market income per household member – by income source (2025)

Source: Singapore Department of Statistics, February 2026.

This asset mix also highlights a potential opportunity.

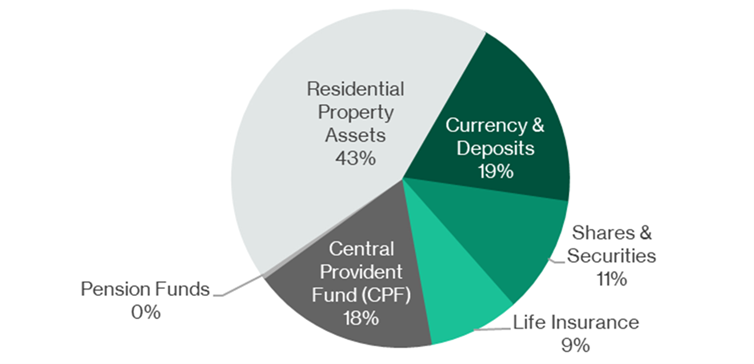

In 4Q25, residential property remained the largest household asset at 43 percent, followed by currency and deposits at 19 percent, and CPF at 18 percent. Direct market exposure was smaller, with shares and securities accounting for 11 percent and life insurance at 9 percent.

In other words, Singapore households are more affluent today, with much of that wealth concentrated in property, largely due to the Government’s home ownership policies over the years4.

At the same time, Singapore households have also built significant wealth in low-risk financial assets like cash and deposits.

The magnitude of wealth held in cash and deposits is vast at $705bn, which is almost as large as the total value of goods and services that the Singapore economy produces in a year, and is around $470,000 per resident household on average5.

Figure 4: Singapore household asset breakdown (4Q 2025)

Source: Singapore Department of Statistics, February 2026.

Compared with regional peers such as Taiwan, whose households allocate around 20.5% of financial assets (based of financial ownership) to equities – as of end 2023, according to Taiwan Directorate-General of Budget, Accounting and Statistics (DGBAS), April 2025, Singaporeans have under-allocated, with a smaller proportion of their wealth exposed to equities, funds, and other financial assets historically.

While this more cautious approach has helped support financial stability, given the vast cash holdings of Singapore households, there is some room for greater equity participation over time.

As interest rates adjust over time and become potentially less attractive, some investors may start looking to put their excess cash to work to provide alternative sources of income and long-term growth.

Even a gradual shift of cash savings into equities could provide an additional source of demand for Singapore-listed stocks, helping to support trading activity, liquidity, and potentially, valuations.

#2 – Global wealth is flowing into Singapore, supporting market confidence

At the same time, alongside rising domestic wealth in Singapore, it is also attracting a growing share of global capital.

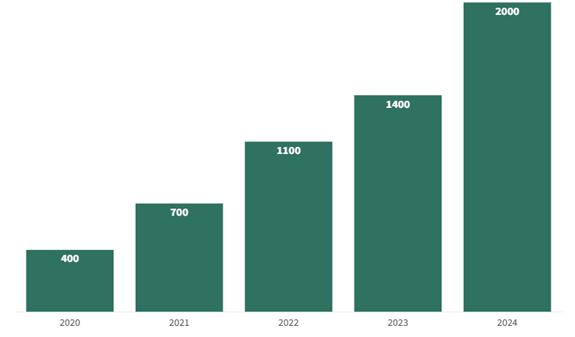

One of the clearest signs is the sharp rise in family offices, with numbers increasing from about 400 in 2020 to more than 2,000 in 2024. This highlights how quickly Singapore has become a preferred destination for wealth management in Asia.

This trend is also supported by stronger cross-border wealth flows. According to Boston Consulting Group’s Global Wealth Report 2025, Singapore recorded one of the fastest growth rates among global financial centres in 2024, with inflows coming from China, India, Southeast Asia, and increasingly the Middle East.

These inflows are also showing up in the banking system. Bloomberg reported that Singapore’s three largest banks attracted S$77 billion of net new wealth money last year6, as wealthy individuals and families shifted more assets here amid rising geopolitical and trade uncertainty.

Figure 5: Singapore’s Digital Enterprise Blueprint (Focus Areas)

Source: Monetary Authority of Singapore, February 2025. Note:

1. Based on number of Single Family Offices (SFOs) awarded tax incentives

2. MAS has noted it does not have authoritative data on the total number of SFOs or the full scale of their operations, as SFOs typically do not manage third-party monies and are generally not required to be registered or licensed. However, MAS does track the subset of SFOs that are awarded tax incentives.

Singapore’s high-net-worth pool is also continuing to grow, adding to the depth of capital in the market.

According to UBS’ Billionaire Ambitions Report published in December 2025, Singapore is home to 55 billionaires, including six new additions in 2025, with their combined wealth rising 66.4 percent to US$258.8 billion. This makes Singapore the third largest billionaire wealth market in Asia Pacific, after China and India.

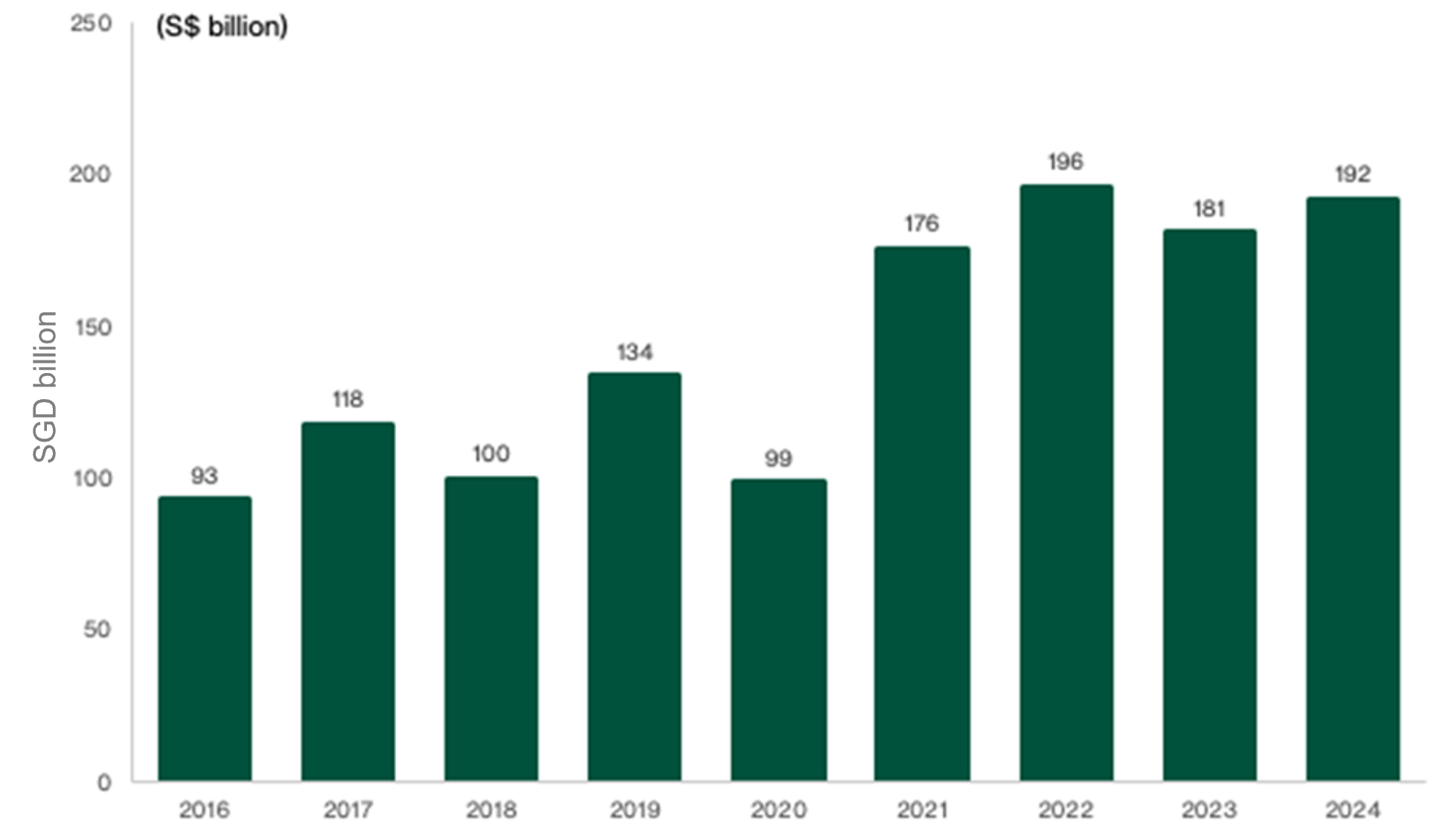

At the same time, broader capital inflows remain strong. Foreign direct investment into Singapore reached S$192 billion in 2024, up 5.6 percent from the previous year, according to the Department of Statistics.

Figure 6: Strong Foreign Direct Investments into Singapore (SGD billion)

Source: Department of Statistics, April 2025.

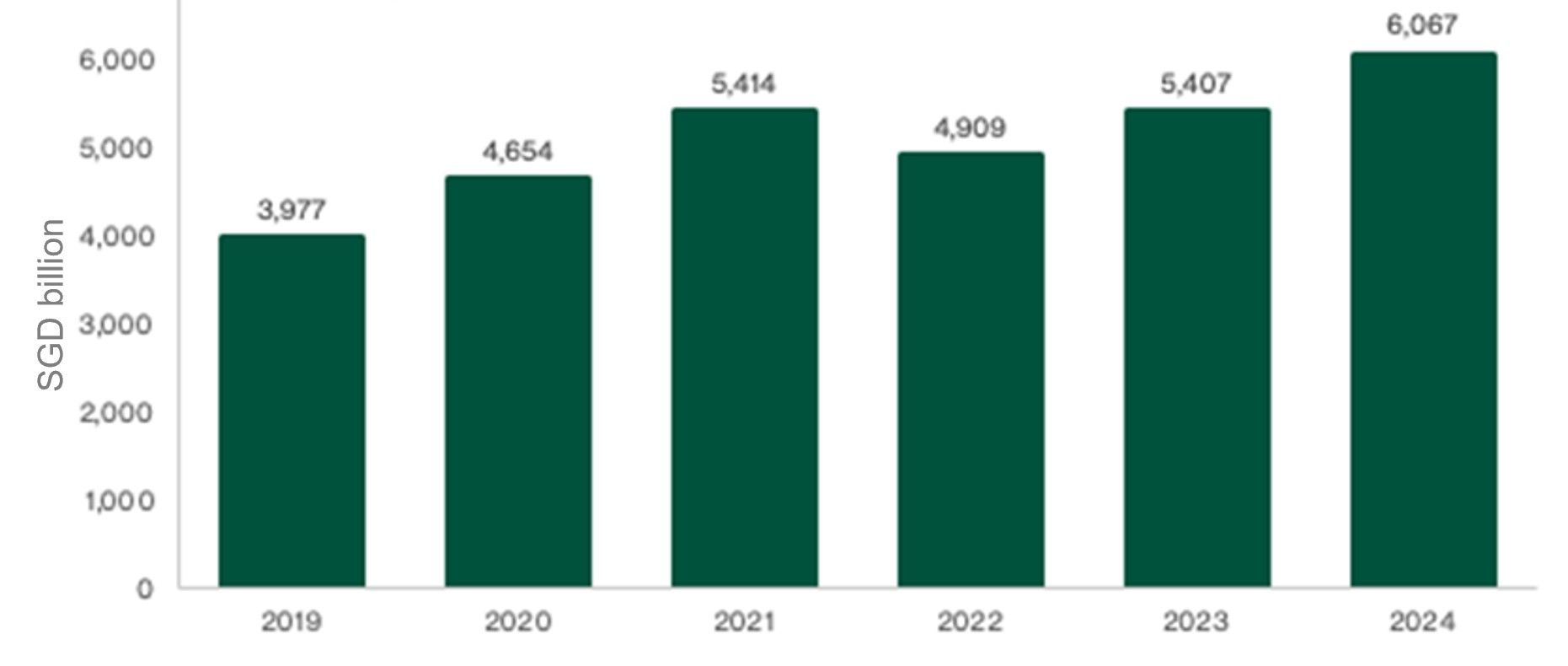

Institutional capital is also growing. The MAS Singapore Asset Management Survey in July 2025 showed that assets under management rose 12 percent to S$6.07 trillion in 2024, while net inflows jumped 50 percent year on year to S$290 billion.

Figure 7: Singapore Green Plan 2030

Source: Monetary Authority of Singapore, July 2025.

Taken together, these trends point to a deeper and more sophisticated pool of capital building in Singapore.

MAS has highlighted that Singapore’s appeal as an investment destination rests on strong fundamentals, including political stability, the rule of law, and a trusted regulatory environment (traits that are increasingly sought in a turbulent Realpolitik world). The city’s deep ecosystem of access to financial, legal, and wealth management services also makes it an attractive base for long term capital growth and wealth planning.

For retail investors, these inflows matter not just because they bring more capital into the market, but because they also reflect confidence from sophisticated investors. As global capital allocates more to Singapore, it can support liquidity, attract greater research coverage and analyst attention, and encourage more corporate activity.

This means retail investors are no longer investing in isolation, but in a market that is increasingly supported by institutional capital.

#3 – More wealth means more liquidity and more opportunities for investors beyond Singapore blue-chips

When both domestic savings and foreign capital increase, markets tend to become deeper and more vibrant.

Higher liquidity can make it easier for companies to raise capital, invest, and grow. It can also improve trading conditions, with tighter bid-ask spreads and broader participation across more stocks.

Singapore’s market has long been associated with banks, REITs, and large government-linked companies. While these remain important, stronger capital flows could gradually broaden investor interest to newer industries and emerging growth stories.

For retail investors, this means opportunities may expand beyond traditional income stocks to include companies with long term structural growth potential.

Key risks to consider

Rising wealth can support Singapore’s market, but it does not guarantee higher share prices.

Changes in global tax rules or regulation could slow the pace of foreign wealth flowing into Singapore. At the same time, local investors may still prefer cash and property, which means any shift into equities could take time.

In the near term, external shocks such as geopolitical tensions or a global slowdown could also weigh on liquidity and investor sentiment.

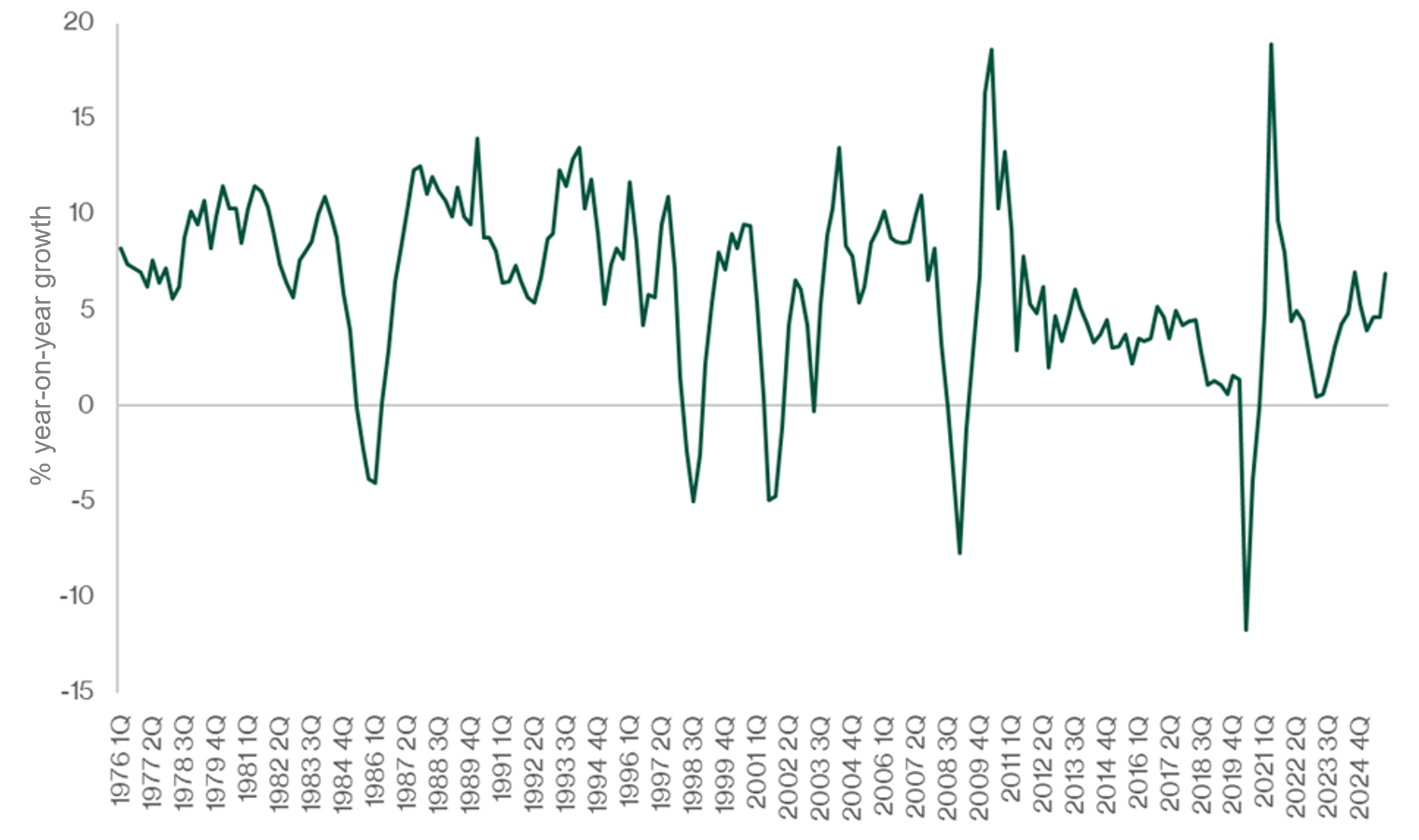

Figure 8: Singapore quarterly real GDP growth, year-on-year (% y-o-y) – still steady

Source: Singapore Department of Statistics, February 2026.

As always, macro tailwinds and economic growth can be cyclical. They may help shape the backdrop, but they are only one part of the investment story. In the end, company fundamentals still matter most.

What could investors do?

The rise in both domestic and foreign wealth adds another layer to Singapore’s long-term growth narrative.

Alongside economic transformation and regional growth, rising capital flows could create a more supportive backdrop for Singapore equities over time.

We would focus on companies that could benefit from deeper liquidity and shifting investor interest. This includes dividend-paying stocks that may continue to attract income demand, as well as companies linked to digitalisation and sustainability trends.

For investors who prefer a more diversified approach, funds that focus on companies improving governance, unlocking value, and participating in Singapore’s changing growth story may be worth watching.

While every investor’s situation is different, Singapore’s growing wealth base suggests the market may be entering a new phase — one shaped not just by economic fundamentals, but also by a larger pool of capital looking for opportunities at home.

1 A timelier estimate of Singapore’s household net worth in 2025 is S$2.2 million per household (a gain of around $220,000 p.a. since 2023), based on data from Singapore Statistics (March 2026).

2 Source: UBS Global Wealth Report 2025.

3 Source: Singapore Department of Statistics, February 2026.

4 Singapore has a home ownership rate of around 90% for resident households which is one of the highest in the world. Source: Population Trends 2025 – Singapore Statistics.

5 Source: as at Q4 2025, Singapore Department of Statistics, March 2026.

6 Source: Bloomberg, “Singapore Banks Draw USD 61 Billion in New Wealth From Asia’s Rich”, February 2026.

Important Information

No offer or invitation is considered to be made if such offer is not authorised or permitted.

This publication is for information only and your specific investment objectives, financial situation and needs are not considered here. The value of units in the Fund and any accruing income from the units may fall or rise. Any past performance, prediction or forecast is not indicative of future or likely performance. Any past payout yields and payments are not indicative of future payout yields and payments. Distributions (if any) may be declared at the absolute discretion of Fullerton Fund Management Company Ltd (UEN: 200312672W) (“Fullerton”) and are not guaranteed. Distribution may be declared out of income and/or capital of the Fund, in accordance with the prospectus. Where distributions (if any) are declared in accordance with the prospectus, this may result in an immediate reduction of the net asset value per unit in the Fund. Applications must be made on the application form accompanying the prospectus, which can be obtained from Fullerton or its approved distributors. You should read the prospectus and seek advice from a financial adviser before investing. If you choose not to seek advice, you should consider whether the Fund is suitable for you. The Fund may use or invest in financial derivative instruments. Please refer to the prospectus of the Fund for more information.

This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

This advertisement is the result of a paid partnership between Beansprout and Fullerton Fund Management Company Ltd (UEN: 200312672W).

The audio(s) have been generated by an AI app