China’s economic importance and the wide breadth and depth of its equity market

China is of huge economic significance, being the second largest economy in the world1. With over 5,0002 listed companies on its domestic equities market and a combined value of over USD 11 trillion3, this space offers significant variety, depth, and access to meaningful growth opportunities.

Why China now?

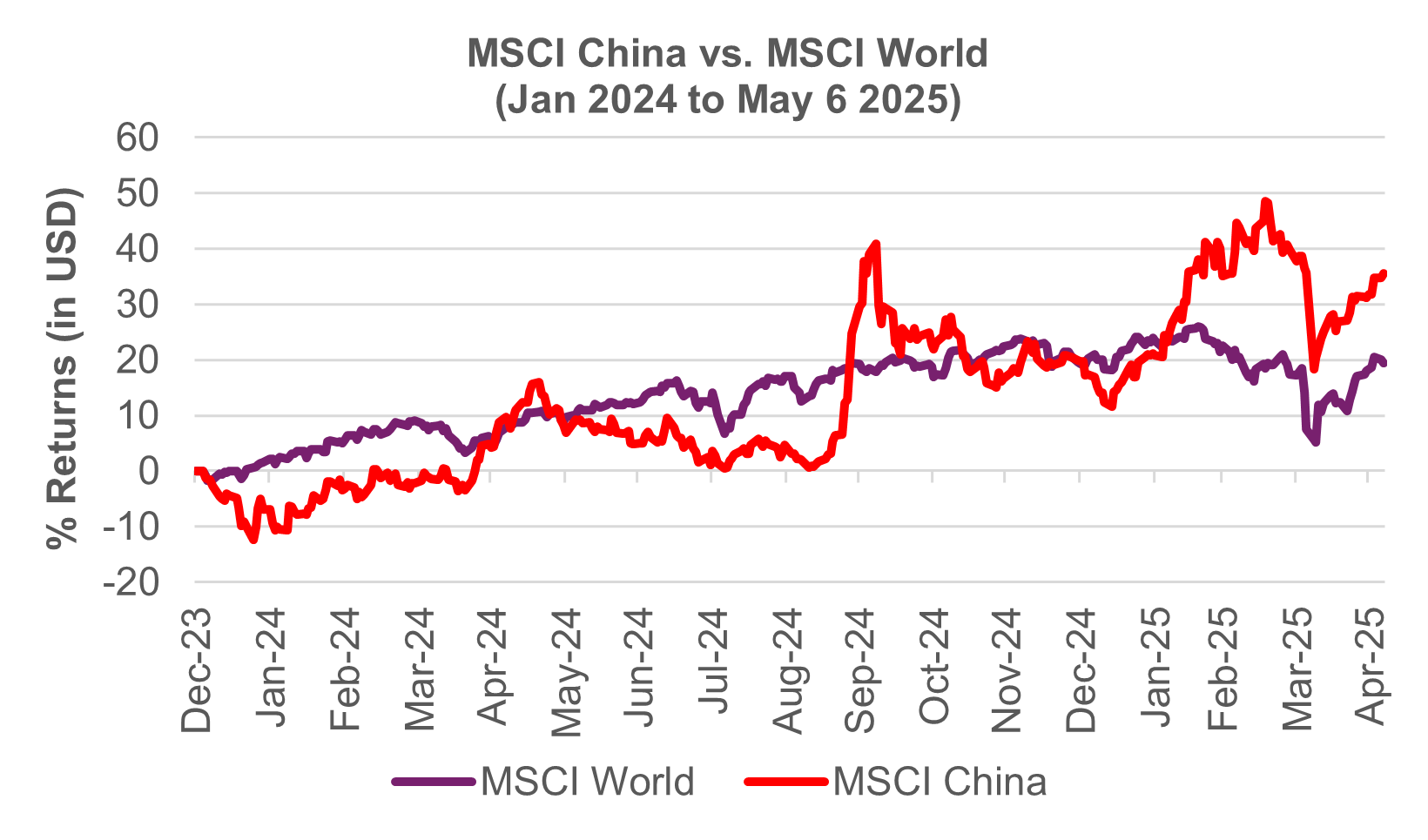

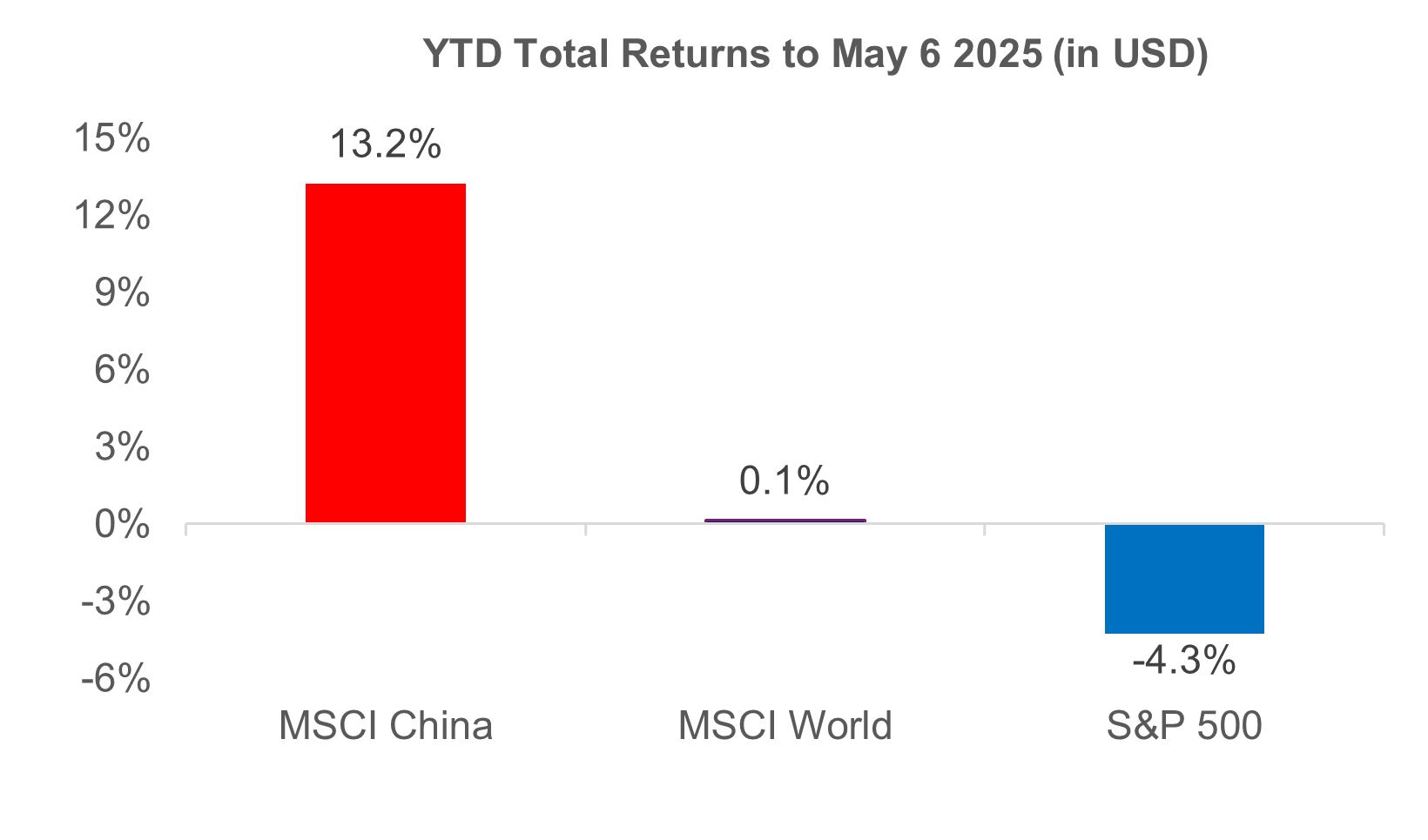

Chinese equities have staged a strong comeback in 2024 and year-to-date in 2025.

Source: Bloomberg, May 2025.

(1) "Game-changing" stimulus

Sizeable policy stimulus announced in Q4 2024 was a “game changer”. China announced an expansive CNY 12 tril. fiscal stimulus package (9% of GDP) in November 20244, comprising of:

- CNY 6 tril5 Local Government Special Bond (LGSB);

- CNY 4 tril6 of existing LGSB quota re-assigned to a debt-swap from 2025-2028; and

- CNY 2 tril7 for shanty-town debt repayments.

Economic targets released at the March 2025 National People's Congress (NPC) were ambitious, and the government is committed to defending these goals.

Source: NPC government work report, March 2025.

(2) Domestically-oriented nature: could be insulated from external shocks

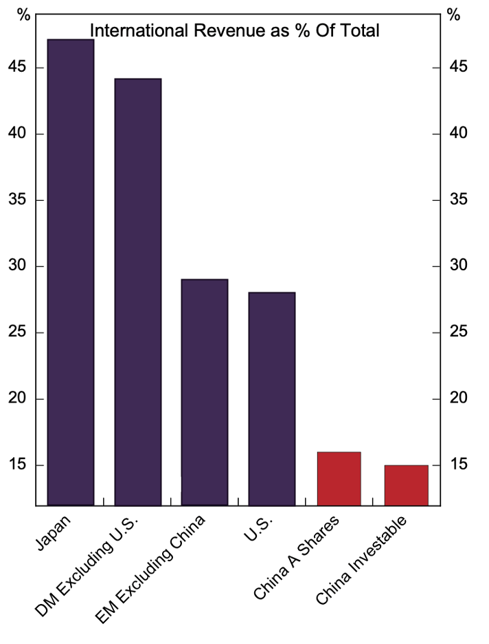

Global geopolitical re-alignment has led to China being increasingly differentiated, less correlated, and more dependent on domestic drivers rather than external factors.

Chinese equities are increasingly domestically-oriented, with only about 15-16%8 of its companies’ revenues derived from international sources, making it resilient and potentially more insulated from external shocks. Given this trait, the direct impact from trade headwinds on Chinese companies’ earnings is expected to be relatively mild.

Chinese companies' exposure to international revenue small vs. other Developed and Emerging Markets

Source: Fullerton, MSCI, March 2025.

Chinese equities have outperformed global and US equities YTD to May 6 2025 amid “Reciprocal Tariffs” headwinds

Source: Bloomberg, May 2025.

(3) Attractive valuations

Having been largely overlooked and under-owned by the international community for the most part from 2021-2023, its valuations now are meaningfully attractive – hovering near historical lows and considerably “cheaper” versus its regional and global peers.

Attractively valued Chinese equities vs. other Developed and Emerging Markets

Source: Fullerton, MSCI, March 2025.

Why Fullerton Fund Management (“Fullerton”)?

“Fullerton” established its China office in 2007 and has managed domestic China A shares for close to two decades. To further build our presence in this market, we have entered a strategic partnership with the investment advisor, Da Cheng International Asset Management Company Limited to bring together Fullerton’s international distribution network and Dacheng Fund Management Company Limited’s investment expertise to global investors.

Dacheng Fund Management Company Limited, founded in 1999, is an experienced Chinese equity market investment manager. It was one of the first ten fund management companies approved and granted a license to enter China’s retail fund management space, and one of four equity managers approved by the National Council for Social Security Fund, to manage Social Security Pension Portfolios9.

With its long-term focus on sustainable returns, and emphasis on a team-based research culture to driving investment performance, its “on the ground” presence and market proximity appropriately positions it to deliver alpha on this front.

1 Source: World GDP (current prices), 2025, IMF.

2 Source: China Association for Public Companies, November 2024.

3 Source: CEIC data, February 2025.

4, 5, 6, 7 Source: NPC government work report, March 2025.

8 Source: MSCI, March 2025.

9 Dacheng Fund Management Company Limited.

No offer or invitation is considered to be made if such offer is not authorised or permitted. This is not the basis for any contract to deal in any security or instrument, or for Fullerton Fund Management Company Ltd (UEN: 200312672W) (“Fullerton”) or its affiliates to enter into or arrange any type of transaction. Any investments made are not obligations of, deposits in, or guaranteed by Fullerton. The information contained herein has been obtained from sources believed to be reliable but has not been independently verified, although Fullerton believes it to be fair and not misleading. Such information is solely indicative and may be subject to modification from time to time. The contents herein may be amended without notice. Fullerton, its affiliates and their directors and employees, do not accept any liability from the use of this publication.

Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express or implied warranties or representations with respect to such data (or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect to any of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling, computing or creating the data have any liability for any direct, indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted without MSCI's express written consent.